Lights, Camera, Tax Credits: How Smart Producers Are Cashing In on the 2026 Film Industry Comeback

The Industry Is Back — and the Numbers Prove It

After years of strikes, streaming pullbacks, and pandemic-era contraction, the entertainment industry is showing unmistakable signs of recovery. Year-to-date domestic box office ticket sales are running more than 20% ahead of the same point in 2025, with industry analysts projecting the domestic box office could reach $9.9 billion in 2026 — its strongest performance since before the pandemic.

Feature film shoot days in California alone increased more than 52% year over year in Q1 2026. TV drama shoot days were up more than 40% over the prior quarter. This isn't a blip — it reflects both a stronger content slate and renewed audience demand for theatrical entertainment.

What's driving the momentum? In part, it's smarter production economics — and at the heart of that is a dramatically revamped state-level tax incentive landscape. States are locked in an aggressive competition to attract film and television dollars, and the result is a historic expansion of available credits, rebates, and incentive programs.

Section 181 Is Gone — Here's What That Means for You

Before diving into state incentives, it's important to understand a significant federal-level shift: Section 181 of the Internal Revenue Code, which for two decades allowed producers to immediately deduct qualified film, television, and live theatrical production costs in the year they were incurred, expired on December 31, 2025, and has not been reinstated.

For productions that commenced principal photography before December 31, 2025, grandfathered Section 181 benefits may still apply to costs incurred in 2026 and beyond — but this requires careful documentation and structuring. For new productions beginning in 2026, the landscape has fundamentally shifted.

The One Big Beautiful Bill Act (OBBBA), signed into law July 4, 2025, did expand Section 181 to include qualified sound recording productions (up to $150,000 immediate expensing), and permanently reinstated 100% bonus depreciation for qualified property acquired after January 19, 2025. Bonus depreciation remains an important tool — but it works differently than Section 181, with deductions tied to when a project is placed in service (i.e., released), rather than when costs are incurred.

The bottom line: the federal incentive framework has changed dramatically, and productions that operated under Section 181 planning assumptions need to revisit their tax strategy with a qualified entertainment accountant immediately.

The State Incentive Gold Rush: Who's Competing for Your Production

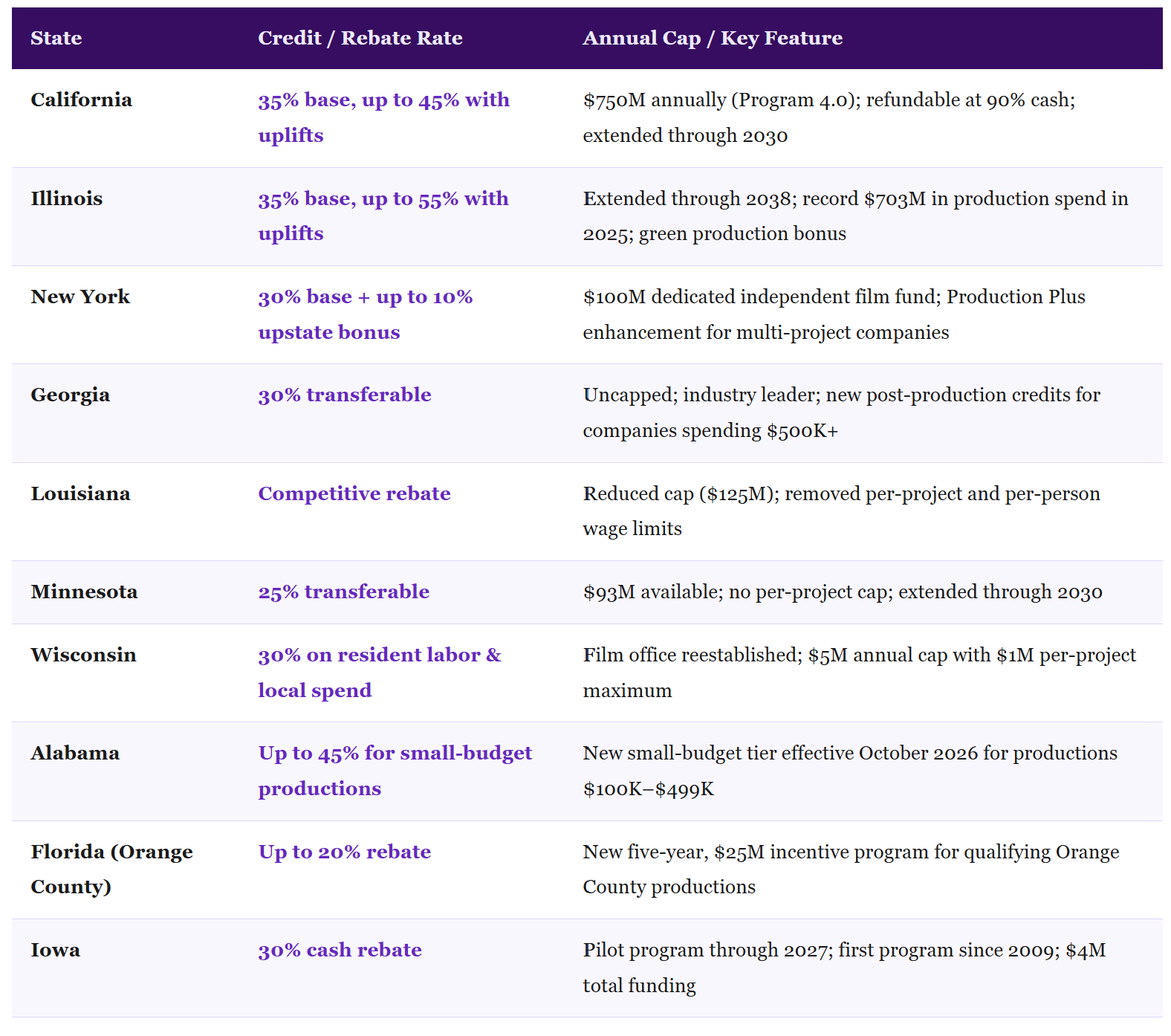

With the federal safety net significantly reduced, state-level incentive programs have never mattered more — and the competition among states to attract production dollars has never been more intense. Here's a snapshot of where the major players stand in 2026:

StateCredit / Rebate RateAnnual Cap / Key Feature

How to Think About State Incentives Strategically

Selecting a filming location based purely on where the story is set — or where it's most convenient — can leave massive amounts of money on the table. Smart producers treat state incentive programs as core budget decisions, not afterthoughts. Here's how to approach the analysis:

1. Understand the Type of Incentive

Not all incentives work the same way. Tax credits reduce your state tax liability dollar-for-dollar — some are transferable (you can sell them to a third party for cash), and some are refundable (the state pays you cash if your credit exceeds what you owe). Rebates are direct cash payments after production and audit. Understanding which mechanism applies changes your cash flow planning significantly.

2. Model the "Jobs Ratio" or Qualifying Spend Thresholds

Most state programs tie credit amounts to qualified in-state spending — labor, vendors, location fees, and services performed within the state. California's program, for example, uses a Jobs Ratio calculation that measures your qualified wages relative to the credit amount. Structuring your production to maximize qualified in-state spend can dramatically increase your incentive return.

3. Look for Stackable Uplifts

Many states layer additional credits on top of the base rate. Illinois offers up to a 55% effective credit rate when you stack base credits with uplifts for hiring from economically disadvantaged areas and "certified green production" status. California adds 5% bonuses for filming outside the 30-mile studio zone or for certain production types. These stackable elements reward producers who plan ahead.

4. Factor in Audit Timelines

State film incentives almost universally require a post-production CPA audit to certify qualified spend before credits or rebates are issued. Audit and payout timelines vary significantly by state — from a few months to 18 months or more. Cash flow models must account for this delay, especially for independent productions with tighter financing structures.

5. Plan Your Entity Structure Early

Production entity structure — whether you're using a loan-out company, a single-purpose LLC, a partnership, or a C-corp — has major implications for how incentives flow through to the principals. This is not a decision to make at the end of production. It needs to be part of pre-production financial planning.

Bonus Depreciation: The Federal Tool Still in Play

While Section 181 has expired, the OBBBA's permanent reinstatement of 100% bonus depreciation for qualified property (including qualified film, television, and live theatrical productions) remains an important federal planning tool for 2026. The key difference: bonus depreciation is claimed when a production is placed in service (released), not as costs are incurred. For multi-year productions, this distinction significantly affects timing and tax planning strategy.

Productions should also note that the 2026 bonus depreciation rate for certain property is 20% — with the full 100% applying to qualified property acquired after January 19, 2025. Working with an accountant who understands the interplay between bonus depreciation, state credits, and your entity structure is essential to capture full benefit.

Frequently Asked Questions???

Is Section 181 completely gone for 2026?

Section 181 expired December 31, 2025 and has not been reinstated. However, productions that commenced principal photography before that date may still access grandfathered Section 181 benefits on costs incurred in 2026 and beyond — subject to documentation requirements. The CREATE Act (currently pending in Congress) would extend Section 181 through 2030, but it has not been enacted as of this writing. Consult a qualified entertainment tax specialist to assess your specific situation.

Can I stack state film tax credits with federal bonus depreciation?

In most cases, yes — state incentives and federal bonus depreciation operate on separate tracks. However, the interaction between them can affect your overall tax picture and entity structure decisions. Proper planning ensures you're not inadvertently creating tax complications when claiming both.

What's the difference between a transferable credit and a refundable credit?

A transferable tax credit can be sold to a third party who uses it to offset their own state tax liability — useful if your production company doesn't have sufficient in-state tax liability to absorb the credit. A refundable credit means the state will pay you cash for any credit amount exceeding your tax liability. Georgia's credits are transferable; California's Program 4.0 is refundable at 90 cents on the dollar. Knowing which type you're receiving changes how you value and plan around the incentive.

Do I need a CPA to claim state film tax credits?

Virtually all state film incentive programs require a third-party CPA audit of qualified production expenditures as a condition of receiving the credit or rebate. Iowa's new program explicitly requires third-party CPA review. Beyond the audit requirement, the complexity of maximizing credit eligibility, entity structuring, and multi-state compliance makes ongoing CPA involvement — with entertainment industry expertise — essential for any serious production.

My production films across multiple states. How do we handle multi-state incentive planning?

Multi-state productions are among the most complex incentive planning scenarios. Each state's program has different qualified spend definitions, minimum thresholds, application windows, and compliance requirements. A tax strategist experienced in entertainment industry multi-state work can help you model production splits, entity structures, and application timing to maximize total incentive capture across jurisdictions.