The Most Expensive Mistake Staffing Companies Make — & How to Fix It Before an Audit

Ask any experienced staffing executive what keeps them up at night, and worker classification is almost always on the list. It's not because the rules are new — it's because the consequences have never been more severe, the definitions have never been more contested, and the enforcement has never been more active.

In 2026, that pressure intensified significantly. Federal regulators — both the IRS and the Department of Labor — have tightened their definitions of who qualifies as an employee versus an independent contractor, increased penalties for wage-and-hour violations, and ramped up audit activity specifically targeting industries with high contingent workforces.

Staffing companies are ground zero for this scrutiny. By the nature of what you do, you place workers at client sites, structure compensation arrangements, and navigate the legal boundary between W-2 employment and 1099 contractor relationships every single day. One systemic classification error — applied across dozens or hundreds of workers — can generate a tax bill that threatens the business.

Here's what changed in 2026, why it matters for staffing, and the steps you should be taking right now.

What Tightened in 2026

The regulatory environment for worker classification has been shifting for several years, but 2026 brought meaningful changes that staffing firms need to understand:

The DOL's Revised Independent Contractor Framework

The Department of Labor has refined its multi-factor "economic reality" test for determining whether a worker is an employee or an independent contractor under the Fair Labor Standards Act (FLSA). The revised framework emphasizes the totality of the working relationship — not any single factor — and has shifted the weight given to factors like worker investment, permanency of the relationship, and the degree of control exercised by the hiring entity.

For staffing companies, this is particularly significant. Workers placed at client sites often have their day-to-day activities directed by the client — not the staffing firm — which can create ambiguity about who is the employer of record and who bears the classification obligation. The revised framework makes it harder to argue that a long-tenure placement who works exclusively for one client under that client's direction is a true independent contractor.

IRS Enhanced Payroll Audit Focus

The IRS has signaled increased examination activity targeting payroll accuracy and worker classification in industries with high contingent workforces. Staffing companies are explicitly in this category. Audits in this space typically focus on whether workers classified as 1099 contractors should have been treated as W-2 employees — and whether the appropriate payroll taxes (FICA, FUTA, SUTA) were withheld and remitted.

State-Level Crackdowns

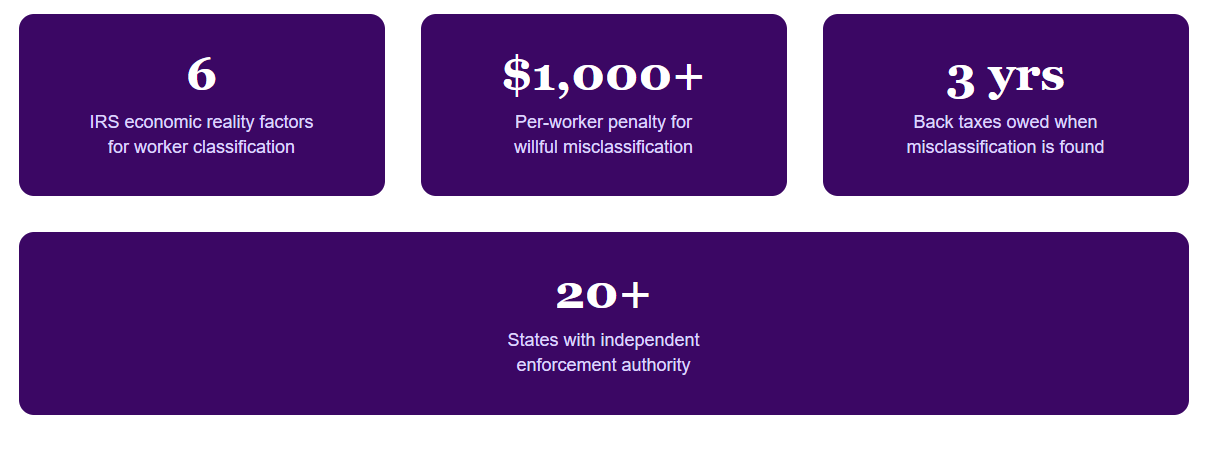

More than 20 states now have their own worker classification enforcement mechanisms — separate from and often stricter than federal standards. Many states use an "ABC test" that presumes a worker is an employee unless the hiring entity can affirmatively prove three conditions. Staffing companies operating across multiple states must navigate a patchwork of standards, and a classification that holds up federally may still trigger state liability.

Why Staffing Companies Face Amplified Risk

Worker classification risk exists in every industry. In staffing, it's amplified by the structural nature of the business:

📙You're in the Middle of a Three-Party Relationship

Most staffing arrangements involve the staffing firm, the worker, and the client. Who controls the worker's day-to-day activities? The client. Who holds the employment relationship? The staffing firm. This structure is legally sound when executed correctly — but it creates natural ambiguity that auditors exploit. If the staffing firm's engagement model looks more like a staffing arrangement than a contractor-client relationship, classification will be challenged.

📙Volume Multiplies the Exposure

A small business that misclassifies one or two workers faces a manageable penalty. A staffing company that systematically misclassifies a category of workers — say, all light industrial day workers placed through one division — faces a penalty structure that can reach hundreds of thousands of dollars or more, plus multi-year back tax liability, interest, and potential civil exposure.

📙The "Safe Harbor" Is Narrower Than It Looks

Section 530 of the Revenue Act provides a safe harbor that allows employers to avoid employment tax liability for worker misclassification if they had a "reasonable basis" for treating the worker as a contractor. That reasonable basis must be documented — a past audit, industry practice, or a legal opinion. For staffing companies, this safe harbor is frequently unavailable because the IRS views them as sophisticated employers who should understand classification rules.

📙Dual Employment Models Create Internal Inconsistency

Many staffing firms run both W-2 placement divisions and 1099 contractor divisions. When workers in functionally similar roles are treated differently for tax purposes across divisions, it creates an audit red flag. Auditors look for patterns of inconsistency — workers doing the same job, with similar oversight, but classified differently depending on which division of the staffing firm placed them.

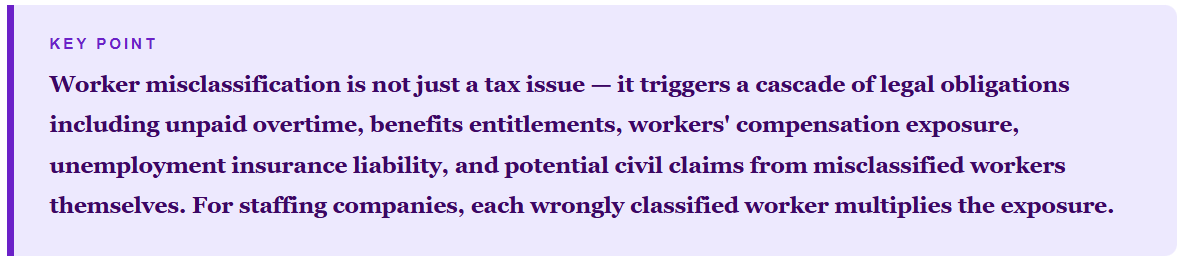

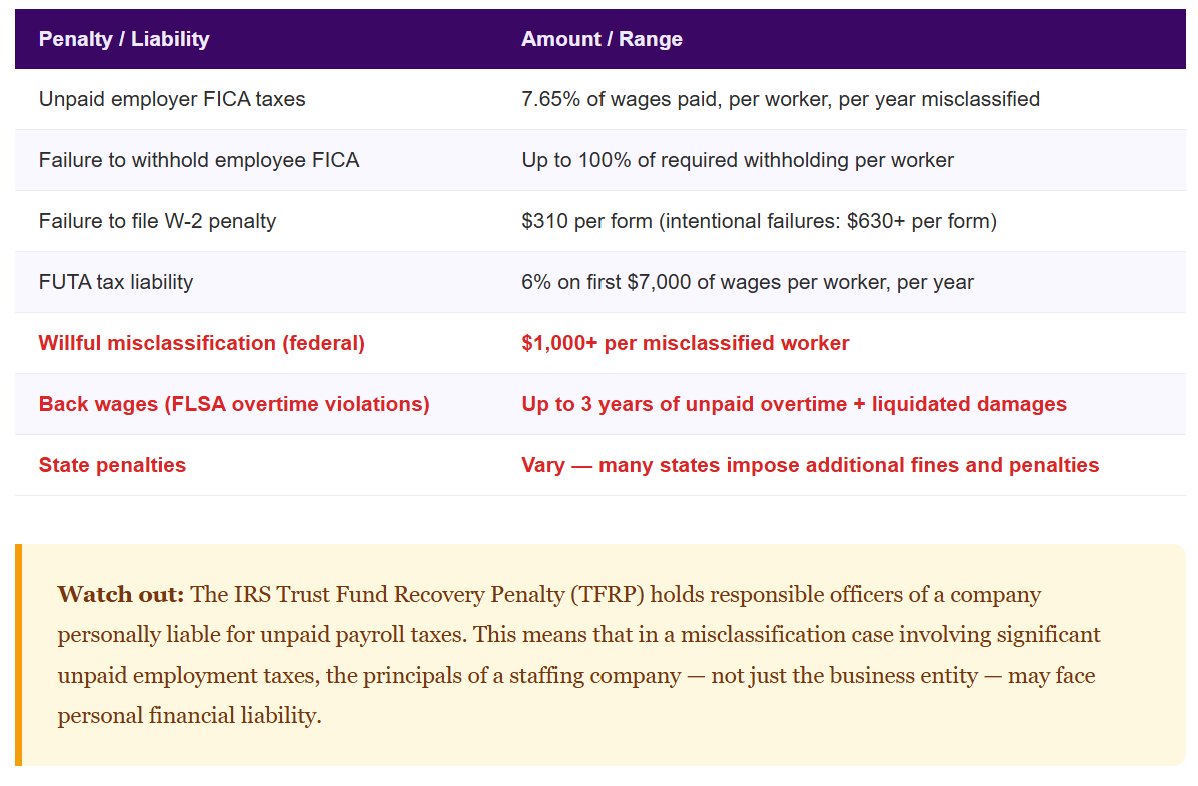

The Penalty Structure: Why Getting It Wrong Is So Costly

The financial consequences of worker misclassification are not modest. When the IRS or DOL determines that workers classified as contractors should have been employees, the following costs typically follow:

The 6 Factors That Determine Classification

Both the IRS and the DOL use multi-factor tests to evaluate worker classification. While the exact factors vary by standard (common law, economic reality, ABC test), the core questions consistently focus on:

Behavioral control: Does the hiring entity control how the worker performs their work — not just the result, but the method?

Financial control: Does the worker have their own business investment, serve multiple clients, and bear financial risk for their work?

Type of relationship: Are there written contracts, benefits, permanency, and is the work central to the business?

Integration: Is the worker's service integral to the core operations of the hiring firm, or is it a specialized peripheral service?

Economic dependence: Is this worker economically dependent on the hiring entity — or are they genuinely in business for themselves?

Permanency: Is the engagement indefinite, or is it a true finite project with a defined deliverable and end date?

For staffing companies, the honest answer to many of these questions often points toward employee status — which is precisely why the industry is under heightened scrutiny.

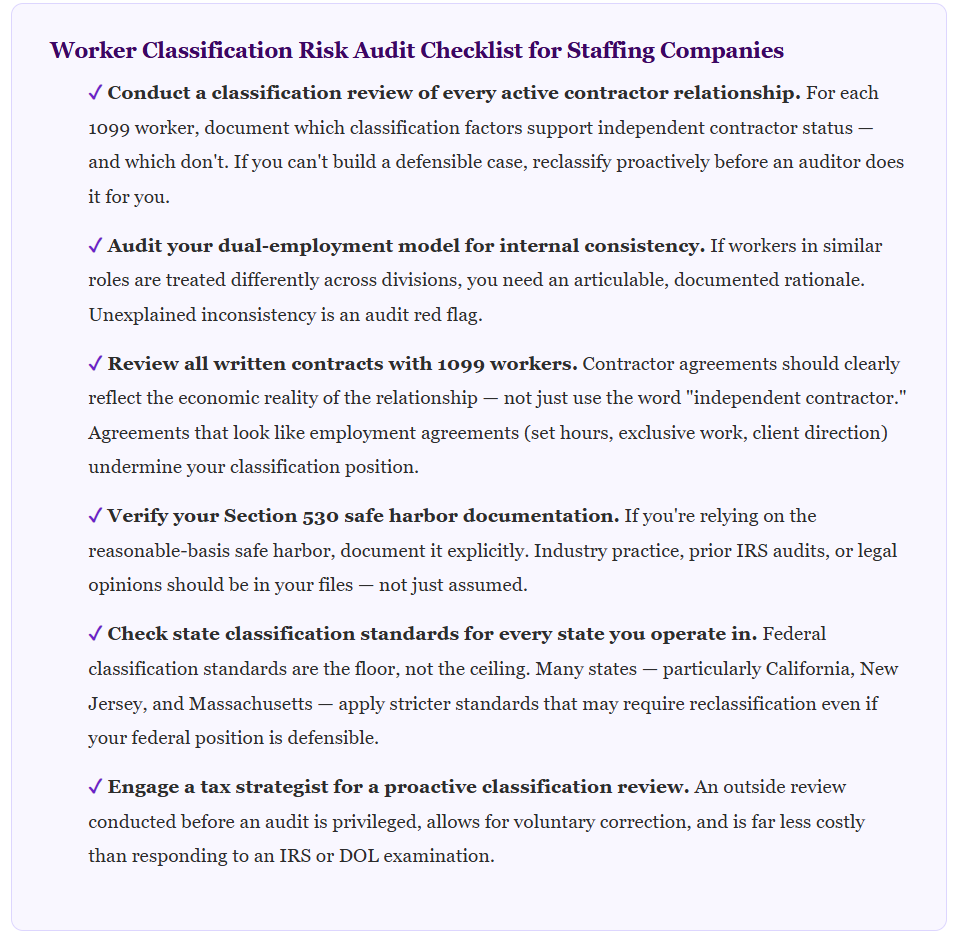

What to Do Before an Audit Finds You

The Strategic Case for Getting Classification Right

It's worth stepping back from the compliance lens for a moment to make the strategic case for proactive classification management.

Staffing companies that systematically misclassify workers are often doing so because the 1099 model is cheaper on the surface — no employer-side payroll taxes, no benefits, no workers' comp premiums. But the math changes dramatically when you factor in audit risk, back tax liability, civil exposure, and the reputational damage of a public enforcement action.

More importantly, the regulatory direction is clear. Federal and state enforcement is intensifying, not moderating. The ABC test is spreading to more states. The DOL's revised economic reality framework makes independent contractor classification harder to defend for long-tenure, single-client placements. The staffing firms that will be well-positioned in five years are the ones building their business models around correct classification now — not scrambling to fix misclassification after an audit.

Correct classification is also a competitive advantage. Clients increasingly want staffing partners who can document their compliance posture. As more sophisticated companies get serious about vendor risk management, the staffing firms that can demonstrate clean classification practices will win business that less rigorous competitors lose.

Frequently Asked Questions

How does the IRS find out we've misclassified workers?

The most common triggers are: a misclassified worker filing for unemployment benefits (which prompts a state agency review); a disgruntled contractor filing a Form SS-8 with the IRS requesting a classification determination; a tip or complaint to the DOL Wage and Hour Division; or selection for a random payroll audit. Staffing companies with inconsistent worker classification practices are more likely to trigger SS-8 filings because misclassified workers who work alongside W-2 employees are more likely to recognize the disparity.

Can we fix misclassification without triggering an audit?

Yes — the IRS Voluntary Classification Settlement Program (VCSP) allows employers to prospectively reclassify workers as employees with reduced tax liability for past periods. To qualify, you must not be under IRS audit, must have consistently treated the workers as contractors, and must have filed all required 1099s. An experienced tax advisor can help you evaluate whether the VCSP is the right path for your situation.

We use written independent contractor agreements. Doesn't that protect us?

Not by itself. The IRS and DOL are clear that labels don't control classification — the economic reality of the relationship does. A written agreement that calls someone a contractor but describes a work arrangement that looks like employment will not provide protection in an audit. What matters is whether the actual working relationship, when examined under the applicable classification factors, is consistent with independent contractor status.

What's the difference between misclassification liability for the staffing firm vs. the client?

In most arrangements where the staffing firm is the employer of record, the staffing firm bears the primary classification and payroll tax liability. However, in cases where the client company exercises significant control over a worker and the IRS determines the client is the "common law employer," the client may share or bear the primary liability. Joint employer arrangements are increasingly scrutinized, particularly in long-term placements.

Is there a federal safe harbor for staffing companies?

Section 530 of the Revenue Act provides a reasonable-basis safe harbor from employment tax liability for misclassification. To qualify, you must have a reasonable basis for treating workers as contractors (based on a prior IRS audit, industry practice, or legal advice), must have consistently treated those workers as contractors, and must have filed all required 1099s. The IRS applies this provision narrowly to staffing companies and requires clear documentation to support the reasonable-basis claim.