Why Your Biggest Client Might Be Your Least Profitable One

The client billing you $800,000 a year might be generating less net profit than one billing $200,000. Most staffing company owners never find out — until a controller review shows them what their revenue is actually hiding.

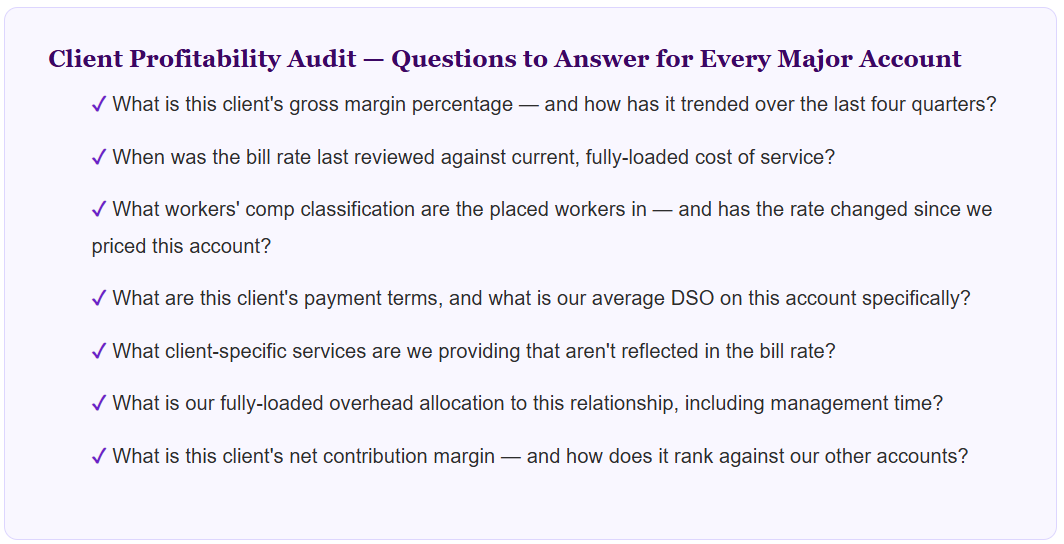

Revenue is the number staffing company owners talk about. It goes on the pitch deck, gets mentioned at industry events, and determines who lands on the "fastest growing" lists. But revenue doesn't pay the bills. Profit does. And in staffing — where gross margins are thin and the gap between gross and net can swing dramatically depending on how a client relationship is structured — the two numbers can tell completely different stories.

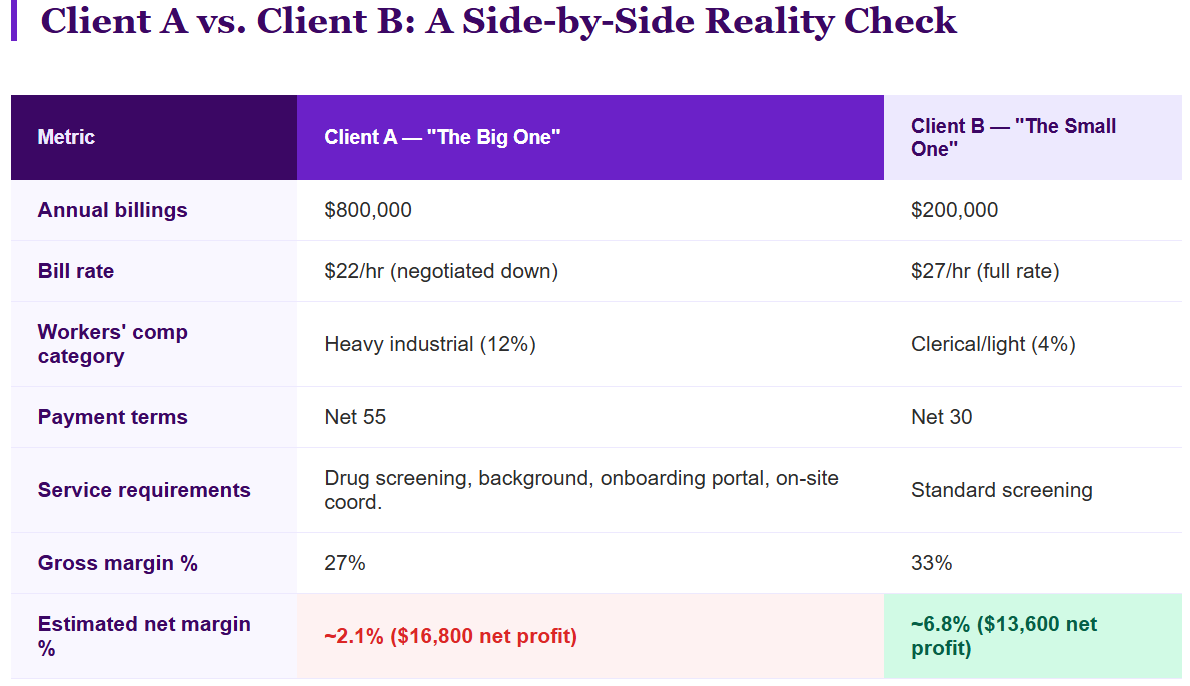

Here's a scenario that plays out more often than most staffing owners would expect: a firm has two clients. Client A bills $800,000 a year and has been a relationship for six years. Client B bills $200,000 and was added eighteen months ago. If you asked the owner which client they'd rather lose, the answer would be obvious — and almost certainly wrong.

Client A is generating a net margin of 1.4%. Client B is generating 6.8%. On an absolute dollar basis, Client B is producing more net profit per dollar billed — and depending on the overhead allocation, may be producing more total net profit on a fraction of the revenue.

This isn't an edge case. It's one of the most common financial patterns in the staffing industry, and it's almost never visible without a deliberate client-level profitability analysis.

The Math Behind the Illusion

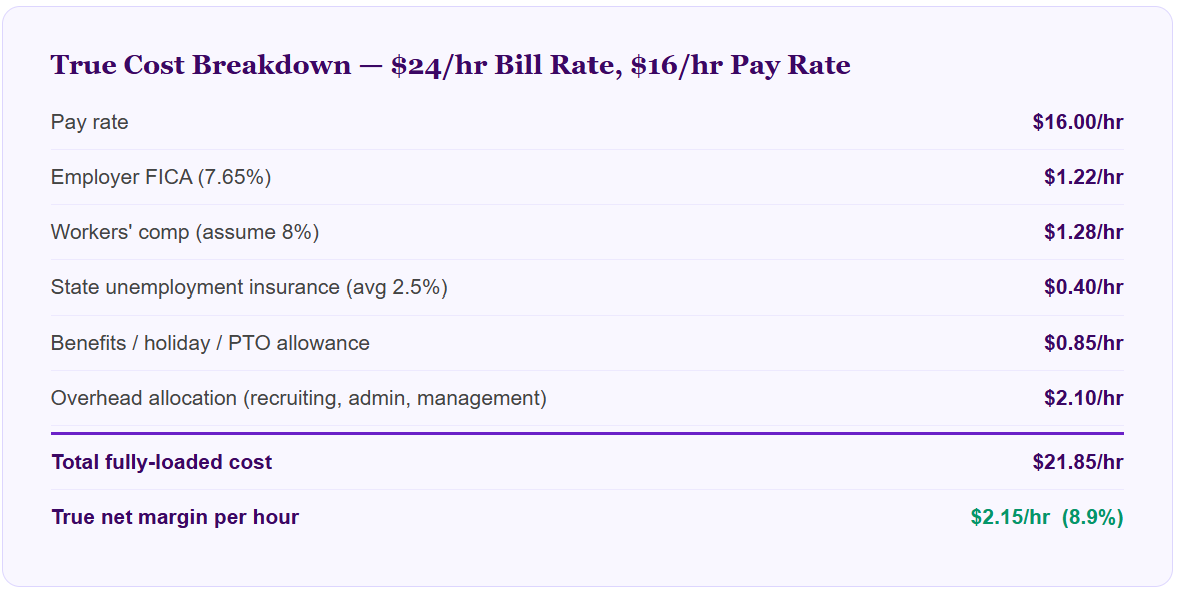

To understand why large clients are often less profitable than they appear, you have to follow the full cost chain — not just the bill rate and pay rate spread.

That's a reasonable margin when the relationship operates at normal parameters. But watch what happens when a few common variables shift:

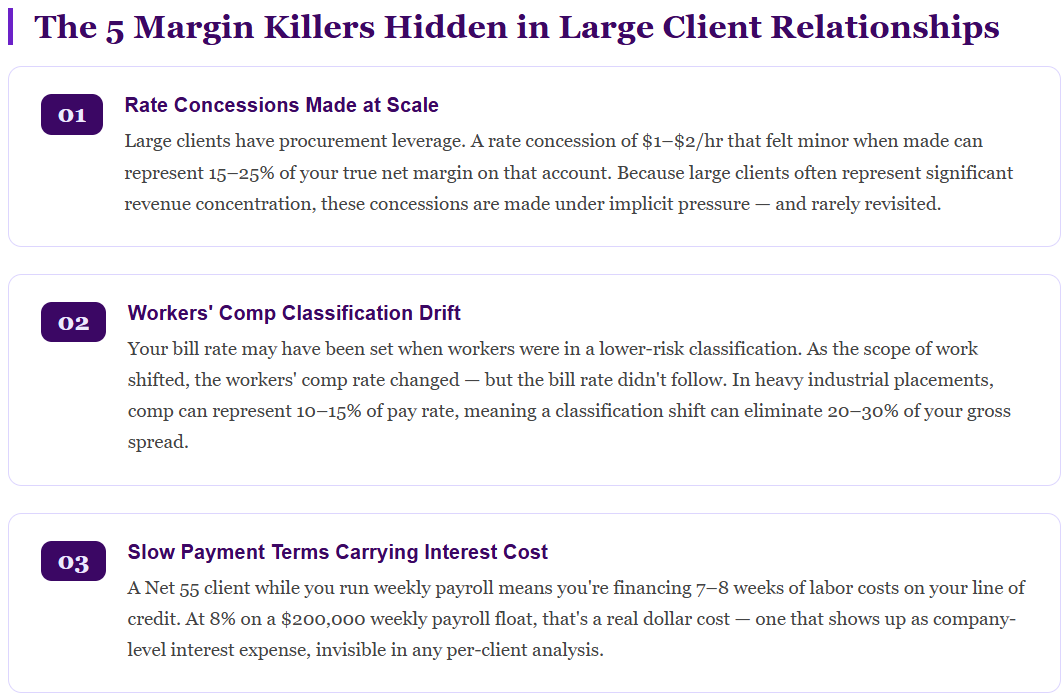

The client negotiated a rate reduction two years ago — your $24 rate is now $22

Workers at this client are in a high-risk workers' comp category — rate is now 12%, not 8%

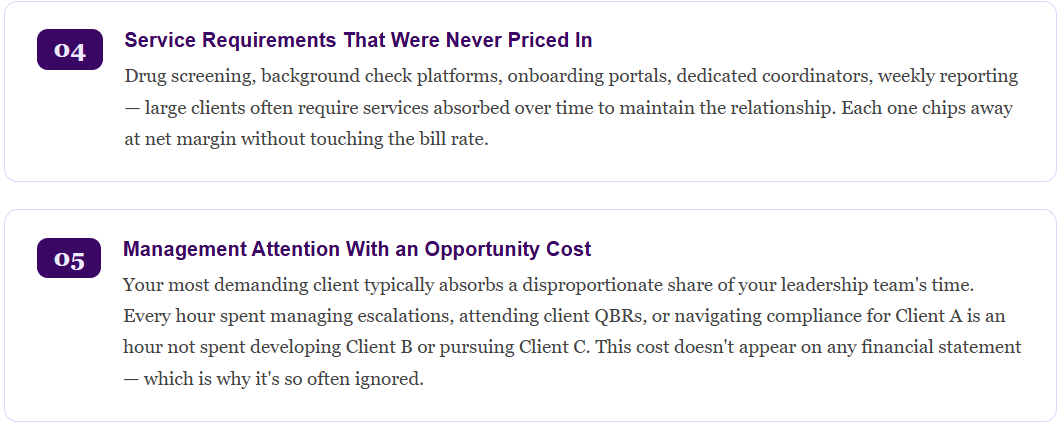

The client requires dedicated on-site coordination — adding $0.60/hr to overhead

This client pays on Net 55 terms — financing 7 weeks of payroll at 8% interest adds ~$0.28/hr

Run those numbers and the "solid" spread is generating approximately $0.47/hr in true net profit — a margin of about 2.1%. Not disastrous, but not what anyone assumed. And certainly not what a revenue-focused view of the relationship would ever reveal.

Client A generates $16,800 in net profit on $800,000 in billings. Client B generates $13,600 on $200,000. Client A bills four times more and produces only 23% more net profit — while requiring significantly more operational overhead, cash management, and management attention. If you replaced Client A's volume with clients like Client B, you'd generate roughly $54,000 in annual net profit on the same revenue. More than three times the return.

What to Do When You Find an Underwater Client

1. Renegotiate the Rate

If your bill rate no longer reflects your true cost of service, you have a legitimate business case for a rate adjustment. The analysis gives you specific data: workers' comp rate changes, market wage increases, inflation in operational costs. Most sophisticated clients understand cost pressures — what they don't respond well to is a rate increase that appears arbitrary.

2. Reduce the Service Burden

If dedicated coordination, premium screening packages, or custom reporting are consuming margin, negotiate which services remain and which get rationalized or priced separately. Not every client needs the same service package at the same bill rate.

3. Accelerate Collections

If payment terms are the primary margin killer, there may be room to offer early payment incentives, negotiate improved terms at contract renewal, or factor receivables from this client specifically. Each improvement in DSO on a large account produces meaningful cash flow impact.

4. Grow the Right Mix Around It

Even if Client A can't be improved, understanding its true contribution changes how you think about growth. Adding $400,000 in revenue from clients with Client B's margin profile does more for your profitability than doubling Client A's volume.

5. Make a Deliberate Retention Decision

Sometimes a large client, despite low margins, provides strategic value — volume that supports fixed overhead, a reference account that opens doors, or a relationship that anchors against revenue concentration risk elsewhere. That's a legitimate conclusion. The difference is making it intentionally, with data, rather than by default.

Frequently Asked Questions

How do I start tracking client-level profitability if my accounting system doesn't do it automatically?

Start with what you have. Even a well-structured spreadsheet that allocates known costs — payroll burden by classification, client-specific services, payment terms — to individual clients gives you 80% of the insight. Your accountant or controller can help set up the right cost allocation methodology and configure your accounting software to capture these dimensions going forward.

What's a healthy net margin target for a staffing client relationship?

It depends on placement type, market, and cost structure — but as a general benchmark, a fully-loaded net contribution margin below 3% on a long-term placement relationship is worth scrutinizing. Temporary light industrial or clerical placements may run 3–6%. Specialized or professional placements should be higher. The trend matters as much as the number — a client at 4% and declining is a different problem than one stable at 3%.

How do I raise the rate without losing the business?

Frame the conversation around cost drivers, not your margins. Come with specific data: workers' comp rate changes, market wage increases, inflation in operational costs. Give appropriate notice. Propose phased adjustments for large relationships. Most sophisticated clients understand cost pressures — what they don't respond well to is a rate increase that appears arbitrary or poorly timed.

Does C2E help staffing companies set up client profitability tracking?

Yes — this is one of the most valuable things we do in advisory engagements with staffing clients. We help set up the right cost allocation methodology, build the client-level analysis, and review it regularly as part of ongoing financial advisory meetings. If you've never seen a client profitability report for your business, a first conversation usually surfaces something immediately actionable.

Disclaimer: This content is for informational and educational purposes only and does not constitute legal, tax, accounting, or financial advice. The examples and figures used are illustrative. Results vary based on individual business circumstances. Please consult a qualified financial professional regarding your specific situation.